Share option pools – what are they and how do they work?

A share option pool is simply an amount of share equity set aside by the company for use in its employee share schemes, such as EMI options; the key point here is that option pool shares don’t exist as such. They are just an undertaking, or promise, by the company’s existing shareholders to issue those shares to employees when options become exercisable, on or before an exit event depending on the option vesting structure. The shareholders are making a commitment that their existing percentage ownership will be 'diluted' by the option pool shares when they are actually issued to employees.

There is no legal requirement to establish an option pool for EMI options or any other type of employee share scheme for a private company. However, shareholders often want to establish a limit on the amount of dilution they may incur as a result of the grant of options to employees. Typically, this is achieved through the rules of the option plan imposing a limit on the number of shares that can be issued through the plan, or a limit is included in a shareholders’ agreement or sometimes in the Articles. The limit could be expressed as a fixed number of shares or as a percentage of the overall share capital.

To explain how the share pool and option process interaction works, here is an example:

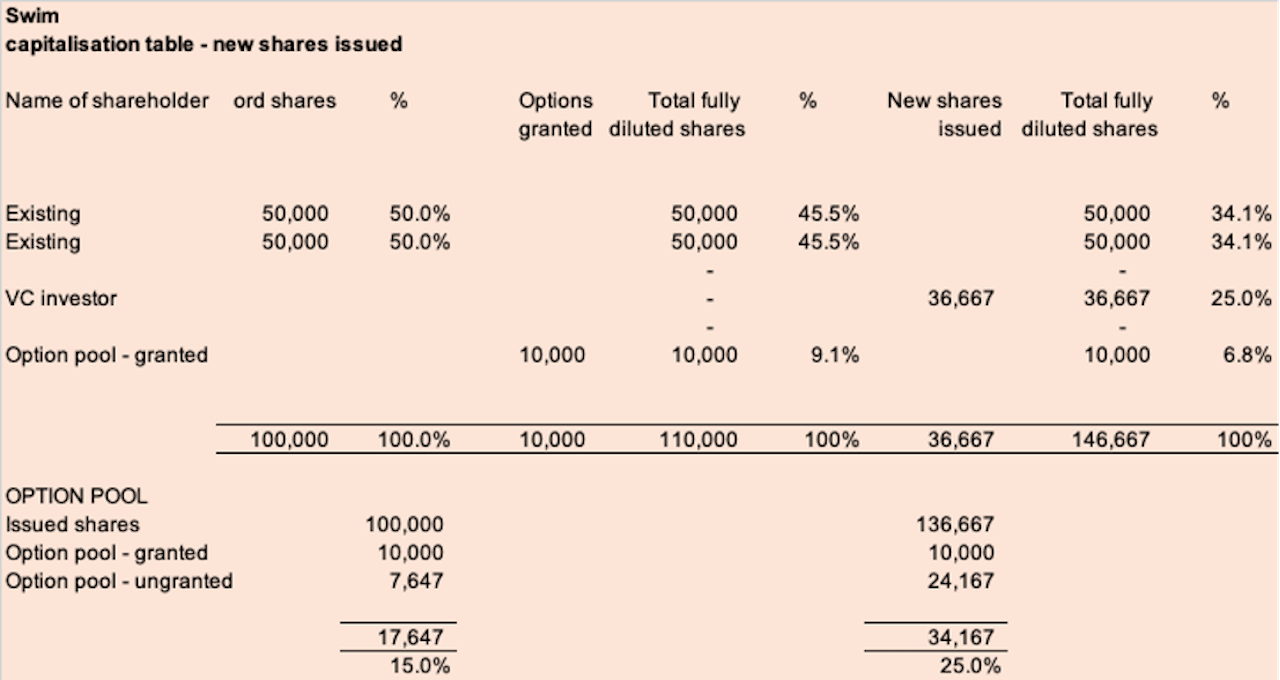

- Swim Limited was set up a year ago and the founders have now employed five staff. They want to set up an EMI scheme so they discuss how much equity they will allow for an option pool

- The founders agree that the pool will be 15% of the company

- Swim has 100,000 issued shares, so a 15% pool would equal 17,647 option shares, calculated by ‘grossing up’ the issued shares (100,000/85%) to get the correct percentage i.e. 17647/117647 = 15%

- The EMI scheme is put in place and Swim grants 5,000 options between the employees. At this point, the company has 100,000 issued shares and 5,000 granted options, with 12,647 ungranted options left in the pool

- The next year, Swim grants another 5,000 options to new additional staff, so the company has 100,000 issued shares and 10,000 granted options, with 7,647 ungranted options left in the pool (at this point, if there was an exit and all employees exercised their options to buy their shares, there would be 110,000 shares bought by the acquirer and therefore the founders would be diluted by 10/110 = 9.1%)- the 7,647 engrafted options just evaporate, as it were, and are not relevant

- Then Swim raises funding from a VC and sells 25% for £2m; the investor gets 36,667 shares, being 25% of the fully diluted equity (110,000/0.75). In the investment agreement that is signed, it is agreed that the option pool is increased to 20% including the 10,000 granted options. The pool is calculated as follows:

a. Issued shares 136,667

b. 20% pool = 136,667/0.8 = 34,167 shares

c. Granted options 10,000

d. Net shares left in pool for future option grants = 24,167

- Note that the VC’s shares were calculated based on 110,000 shares so that they were not diluted by the granted option shares, and effectively they will only be diluted by any future option grants out of the 24,167 left in the pool. The extent to which an investor gets diluted by options is often a key negotiating point during a funding round and for the founders, it’s obviously better if the VC agrees to more rather than less dilution. In our example the VC has agreed to be diluted by the ungranted pool, but many investors will want their equity percentage based on fully diluted shares including both the granted and ungranted option shares

- The number of granted options will increase every time new options are awarded to employees, but if an employee leaves the company they will often lose their option rights and in that scenario their granted option shares revert to being ungranted and go back into the pool so that they can be used again

- This example is illustrated numerically in the table below

How large should an option pool be?

A typical range for an EMI scheme is 5% to 20% of the fully diluted share capital. Often it may start as 5% to 10% but then is increased as the company becomes more valuable, because the founders recognise that their share of the exit sale proceeds in cash terms is expanding over time, even if they get more diluted by further option grants.

It's also worth a look at this blog by Fred Wilson, a seasoned US VC: https://avc.com/2009/11/valuat...